The Arun Bajoria: Bombay Dyeing Tussle

🌐 International Buyers — Pay via PayPal

Details

BECG029

8

2001

YES

0

Hooghly Mills Company Ltd.

Textiles & Apparel

India

Conflicts of Interest,Capital Markets & Investments

Abstract

The case, ‘The Arun Bajoria - Bombay Dyeing Tussle’ provides insights into the events leading to the SEBI decision to bar jute businessman and stock market operator Arun Bajoria to trade in the stock market. The case examines how Arun Bajoria acquired a stake in Bombay Dyeing and also discusses the criticism faced by the regulatory authorities and the problems with the SEBI takeover code.

Learning Objectives

The case is structured to achieve the following Learning Objectives:

- SEBI takeover code.

Contents

“This has hurt my ego. I will exercise my full rights and let them try and see how much nuisance I can create.”

- Arun Bajoria, on his voting rights being frozen by Bombay Dyeing, in November 2000.

“We know how to defend ourselves.”

- Bombay Dyeing sources in October 2000.

In October, 2000, the atmosphere at Neville House, Mumbai, official headquarters of Indian textile major Bombay Dyeing (BD) was extremely tense. The man responsible for this was Arun Kumar Bajoria (Bajoria), chairman of a little known Kolkata based jute company, Hooghly Mills Company Ltd.

Bajoria, a jute dealer-cum-professional stock market speculator, had announced that his equity stake in BD had crossed the 15% limit set in the Securities and Exchange Board of India (SEBI) takeover guidelines. The announcement attracted immense media coverage. BD accused Bajoria of having violated SEBI guidelines, which laid down that once a person?s equity stake exceeded 5%, he had to inform the company concerned. BD lodged a complaint against him with SEBI.

The Bajoria-BD tussle intensified over the next few days, with the Finance Minister Yashwant Sinha saying that the issue had underlined the need for amending the takeover code to make it foolproof. The controversy even divided the chambers of commerce and industry, with ASSOCHAM and CII demanding a review of SEBI's takeover code, while FICCI claimed that Bajoria's stake hike could not be contested if it was in conformity with the existing regulation.

Meanwhile, Bajoria revealed his plans to claim a seat on the BD board and to have Nusli Wadia (Wadia), BD's Chairman removed on charges of mismanagement: “I had filed a case with the CLB under Sections 396 and 397 for mismanagement in BD by Mr. Nusli Wadia and will demand his removal from the Board.” He also demanded the appointment of an external auditor to probe instances of mismanagement by Wadia.

Established in 1879, BD was one of the oldest and largest mills in the Indian textiles industry. The company was promoted by the Wadia family and had been managed by successive generations.

BD's major business comprised textiles (predominantly cotton) and chemicals (DMT - Dimethyl Terephalate, used for fabric manufacturing). The company primarily manufactured and sold cloth, which accounted for 97.4% of the Rs 5.35 billion turnover in 1999-00. In cotton textiles, BD was one of the oldest players in the country dealing in shirting, suiting, sarees, dresses, bed sheets, pillow covers, furnishings, blankets and other readymade garments. The company was also present in the industrial segment where it supplied canvas and other specialty grade cloth made according to users? specifications to canvas shoe manufacturers. BD was one of the leading producers of DMT in India. The company owned five textile units - three at Mumbai (Maharashtra), and one each at Roha (Maharashtra) and Jamnagar, (Gujarat) besides a DMT plant at Patalganga (Maharashtra). The Jamnagar unit had 25,000 spindles and the two Mumbai units had a combined capacity of 137,000 spindles and 1,900 looms.

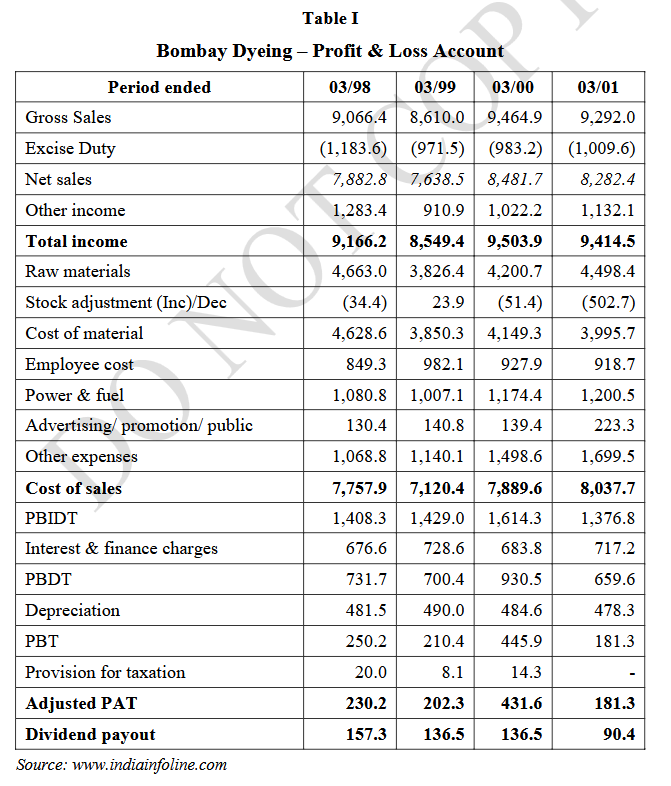

Over the years, BD had built strong brand equity and a well spread out network of retail outlets. However, due to a lack of focus and poor marketing skills, the company saw its competitive position weaken in the Indian textile business. Its backward integration into DMT considerably eroded shareholder wealth. The recessionary conditions in the textiles and apparels market in the late 1990s led to declining margins for the company. (Refer Table I). As a result, in the late 1990s, BD focussed on cost cutting through tighter inventory controls and downsizing.

Bajoria was born in Kolkata in a prominent family of jute businessmen. In the 1980s, when the Kolkata jute business was faring very badly, Bajoria?s companies were generating excess cash. This prompted Bajoria to buy and lease jute mills all over Kolkata. By the mid 1990s, he controlled more than 15% of West Bengal's private sector jute production.

The BD issue was not Bajoria?s first brush with the law. Earlier, he was involved in a case for defaulting on the provident fund dues in one of his jute mills. He had also been put in judicial custody by the Enforcement Directorate regarding irregularities in stock market operations. Bajoria strictly avoided bank funding and depended on internal funding for his stock market and business operations. Bajoria came into the limelight when he bought 10 lakh shares of State Bank of India at Rs 220-225, and made a significant profit later by selling them at high prices.

In June 2000, Bajoria had acquired over 5% of BD's equity through stock market operations. BD at that time was a cash and asset rich company with highly undervalued stocks. This gave Bajoria ample chance to reap substantial returns in the stock markets. (During July 1999-November 2000, BD?s market capitalization ranged between Rs 1.64 billion and Rs 3.28 billion. Taking an average market value of Rs 2.46 billion, the company was quoting at less than a sixth of its actual worth of Rs 14.65 billion according to a November 2000 Business Today report.) BD noticed the acquisition by Bajoria later in June 2000 during a weekly review of transactions in its shares from the depositories. As the company had not received any intimation from Bajoria about this acquisition, it lodged a complaint with SEBI, the Company Law Board (CLB) and the BSE in the first week of July 2000. Bajoria however claimed that he had sent a letter to the company regarding the same, vide a letter dated March 16th 2000. As the issue remained pending with the SEBI, the CLB ordered the voting rights of Bajoria to be frozen until a solution was arrived at. BD sources meanwhile blamed SEBI for the laxity shown in its investigations in the case, as even by the end of the month, there was no response from the market regulator. The company even had to send a reminder to SEBI, prompting Executive Director, S.S. Kelkar to comment, “We have been requesting them to take action under the takeover code. We even requested SEBI to conduct an investigation in terms of Regulation 38 of the SEBI takeover code and issue appropriate directions apart from initiating action under Section 24 of the SEBI Act, 1992. We have already written to them. They should call us.”

The resentment of the Wadias was not difficult to understand. The controversy had come to be seen as a case of a lone stock market operator creating trouble for the company. Though Bajoria made claims of being concerned with BD?s functioning, many believed that he had no interests in the company?s business, and was looking solely to book gains through stock deals. According to a Financial Express report, “The truth is Bajoria is best a turnaround artist who has built a Rs 10 billion business empire buying sick companies at bargain prices and reviving them. A trader of jute goods at most with an eagle?s eye for opportunistic windfall.” There was even speculation that Bajoria was acting on behalf of a big corporate house, which was eyeing BD. Commenting on this, Bajoria said, “Nonsense. And even if I am, so what? I do not think that it is illegal. I know what you mean. And let me tell you, if Reliance approaches me with an offer to buy my holdings in Bombay Dyeing, I will readily sell off the entire lot to Dhirubhai. May be I will sell it cheaper if he comes up with an offer, cheaper than the 200 plus I am determined of getting from whosoever else I sell to, including Bombay Dyeing.”

Bajoria came up with contradictory statements frequently in the media. While at one point he said he was willing to make an open offer for BD shares, later he changed his mind saying, “It does not make sense, simply because it will not give me a controlling stake in the company.” Bajoria also claimed that he had bought a substantial portion of BD shares from Unit Trust of India (UTI). However, UTI officials denied this. Bajoria?s claims of having received offers from Reliance India to buy the BD stake were also proved wrong.

In November 2000, Bajoria announced that he was willing to sell his stake to Nusli Wadia if he paid a good price. However, the Wadias refused to bow down to Bajoria?s tactics and decided to continue the legal battle.

In November 2000, Bajoria was served a show cause notice by SEBI and was asked to respond within 15 days. Bajoria requested an extension. He was later asked to appear for a personal hearing on February 1, 2001. However, just before the due date, he sought another extension from SEBI. The next date was set for February 28, 2001. At this point, Bajoria was asked by the CLB to appear for a hearing in March 2001. Bajoria then moved the Kolkata High Court seeking quashing of the SEBI notice claiming that he had informed BD of his stake acquisition by a letter sent „under certificate of posting.? However, the case scheduled for a hearing on February 28 was postponed to March 5 without the hearing. As a result, the SEBI hearing was stayed till March 2, 2001.

By May 2001, Bajoria had reduced his stake in BD to 4.5% from the October 2000 level of 12%. This move was reported to have hit him hard as from a high of around Rs 132 during October 2000, the BD share had declined by over 68%. Bajoria had begun acquiring the stock at around Rs 45-50 in mid-April 2000, with the average cost of acquisition of the shares being around Rs 70. The prices at which he had to offload the BD scrip were almost 70% below their acquisition price. (However, Bajoria claimed to have sold his shares at an average price of Rs 92-93 each.)

Bajoria was asked to appear before SEBI in June 2001. However, in a letter to SEBI, he said, “Since the issue pertaining to Bombay Dyeing is already with the Company Law Board (CLB), the issue of my personal appearance does not arise.”

In July 2001, the CLB held that Bajoria had violated the provisions of the SEBI takeover code by not disclosing his acquisition of more than 5% shares of BD. The CLB order said, “We find that the letter dated March 16, 2000 cannot be construed to be a 'disclosure' in terms of Regulation.” The CLB said that the letter allegedly sent by Bajoria and his associates on March 16, 2000, informing BD about the acquisition of more than 5% of the company?s shares could not be construed as a disclosure since it was not as per the SEBI prescribed format. Bajoria claimed that he had crossed the 5% mark on March 15, 2000 and this was made known to BD through a letter dated March 16, 2000. While declaring the acquisition of shares in excess of 5%, the court also added that „the possibility of the letter of 16th March having been prepared at a later date could not be ruled out.

CLB said that Bajoria had not furnished any evidence like postage account or a dispatch register and the only proof of him having posted the letter was in the form of a copy of the certificate of posting. Kelkar added that the March 16 date was of no relevance, as according to BD's records, Bajoria's stake at that point of time was well below 5%. The stake crossed the 5% level only on May 16. So even if Bajoria did send a letter dated March 16 to BD, its content could not be about his holding exceeding 5%, simply because it had not exceeded 5% at that time.

By August 2001, Bajoria was reported to have again increased his stake in BD to 6% from 4.9%, as the company revealed plans to opt for a share buyback plan. The buyback offer was for 1.02 crore equity shares, amounting to 25% of BD?s total paid-up equity share capital at Rs 60 per share. Following this, the promoter stake in the company was expected to go up to 54.47% from the August 2001 level of 40.85%. It was rumored that Bajoria?s renewed interest was solely to book profits arising due to a possible price increase led by the buyback news.

Before Bajoria could further increase his stake, towards the end of August 2001, SEBI passed its verdict barring Bajoria and his associates from accessing the capital market and dealing in securities - either directly or indirectly - for one year. Bajoria's broking firms, Mega Stock and Mega Resources, through which the BD deals had been executed, were also barred from trading.

Reacting to the SEBI decision, Bajoria said, “Takeover guidelines have been violated even in the past. In these cases SEBI had merely asked them to pay a fine after warning them against making the same mistake again in the future. But, in my case, the market regulator has taken a harsh decision. The SEBI order is totally malafide. It is a politically motivated decision and not a commercial decision in the true sense of the word.” He announced that he intended to file a writ petition against the SEBI order.

Analysts claimed that the ruling was unlikely to pose any major problems for Bajoria's plans to offload his BD stake through the buyback program. This was because Bajoria was reported to have transferred his shares to various associates and relatives, who would not be affected by the SEBI order, and who could easily sell them in the market. Bajoria said, “I was apprehensive that SEBI might take such a step to prevent me from taking advantage of BD?s buyback. So, I transferred the shares to my associates so that any order barring me, my relatives and my broking firms from entering the markets did not affect my plans.”

As in the case of many other stock market scams, SEBI?s role in the Bajoria/BD tussle was severely criticized. Besides being criticized for not formulating a clear takeover code, SEBI was also accused of delays in taking action against Bajoria after BD lodged the complaint. In fact, it was after the Bajoria case that SEBI made certain amendments to its takeover guidelines. SEBI had begun introducing changes in the takeover regulations in 2000, but it had to shift its attention to investigations following the Ketan Parekh scam in 2001.

In the pre-demat trading days, since the company made the delivery of shares, it could stop the transfer if any irregularities were noticed. However, trading in the dematerialized mode did not allow the companies to block the transfer of the shares and, thus, exposed the companies to risks. The onus was on the acquirer to inform the company that the 5% limit had been crossed. The only way out for a company was to petition SEBI and the CLB to take action against violations. If there were delays in these bodies taking action, there was little the company could do. Even while the BD case was on, Bajoria carried out a similar exercise with the paper major Ballarpur Industries Ltd. (BILT), by picking up a 10% stake in the company. BILT also approached SEBI in this regard after Bajoria approached the company to get a seat on the board. (The matter was put to rest later with Bajoria disposing of his stake.)

Even after barring Bajoria from entering the capital markets, SEBI itself was not too sure whether it would be able to pre-empt such incidents in the future. A top-level SEBI official said, “Even if Bajoria has transferred his shares to friends and associates recently, it is very difficult for SEBI to book him for it. Under the given takeover regulations, it is very difficult to establish them as persons acting in concert and helping him to dodge the suspension.”

1. Study the Bombay Dyeing-Arun Bajoria controversy and prepare a note highlighting the developments during the course of the dispute.

2. "Mismanagement of a company by the promoters justifies its being taken over through open market operations.? Against the backdrop of Bombay Dyeing?s dismal performance over the years, comment on this statement.

3. Critically comment on SEBI?s role in the Bombay Dyeing/Arun Bajoria tussle. Do you agree that the takeover code is still not powerful enough to check such incidents in future? Give reasons to justify your stand.

Keywords

The Arun Bajoria Bombay Dyeing Tussle, SEBI, bar jute businessman, Arun Bajoria, case, Bombay Dyeing, criticism, regulatory authorities, SEBI takeover code

Related Case Studies

| Case Title | Details | Price | Add to Cart |

|---|---|---|---|

|

Case Title PepsiCo India Vs Gujarat Potato FarmersCase Code: ECON074 |

Details | 400 | Add to Cart |

|

Case Title Should Infosys Go Ahead With Share Buyback?Case Code: FINC103 |

Details | 500 | Add to Cart |

|

Case Title Options Strategies on Microsoft and Facebook Stocks (D)Case Code: FINC099 |

Details | 500 | Add to Cart |

|

Case Title Alibaba’s IPO: Father of all IPOsCase Code: FINC094 |

Details | 400 | Add to Cart |

|

Case Title Uber: Rising Valuations Amidst Ethical WoesCase Code: BECG137 |

Details | 600 | Add to Cart |