The Takeover of Raasi Cements by India Cements

🌐 International Buyers — Pay via PayPal

Details

BSTR001

8

2001

NO

0

Raasi Cements Ltd., India Cements Ltd.

Engineering & Construction

India

M&A,Postmerger Integration, Growth Strategy

Abstract

The year 1998 heralded the era of consolidation in a hitherto fragmented cement industry in India. The case study focuses on the takeover of Raasi and Sri Vishnu Cement Limited (SVCL) by India Cements Limited. (ICL). It provides an overview of how ICL increased its stake in Raasi, starting from the mid 1990s. A detailed analysis of the actual takeover looks at the various options that Raasi had, if it wanted to ward off takeover and covers why it was unsuccessful in its attempts to do so. The case is intended for MBA/PGDBM level students as part of the Business Strategy curriculum. The case throws light on how mergers, takeovers and acquisitions can be used as tools for growth and expansion. The case is a good example of a geographic market-extension merger which involves two firms having operations in non-overlapping geographic areas, and rationalization of various markets between the two companies. From the case, students are also expected to understand how consolidation is taking place in the cement industry in India. They will also be able to understand the strategic intent behind taking over a company which produces the same product, cement in this case.

Learning Objectives

The case is structured to achieve the following Learning Objectives:

- Takeovers, mergers, acquisition.

Contents

In January 1998 there was an unusual press conference at Hyderabad's Hotel Viceroy. Seventy-seven-year-old B.V.Raju, (Raju) vice-chairman of the Hyderabad (India) based Raasi Cements (Raasi) mobilized all his daughters, sons-in-law, and grandchildren in a display of family unity. “We are one united family and will ward off any takeover threats. I am a humble, simple man who has always maintained a low profile. But when it comes to fighting, I shall not be found wanting,” he declared.

Raju's comments came in response to reports that N. Srinivasan (Srinivasan), was buying Raasi's share in the market. The Raasi scrip, which hovered around Rs 50 till November 1997, tripled in value to Rs 158 in January 1998. Srinivasan had acquired 18.03% of Raasi shares by January 1998.

While he was responding to the takeover reports Raju recalled, “I made an offer to Srinivasan to buy the shares with a 10 per cent profit margin and 20 per cent interest from the date of purchase. Though he told me he had no ulterior motives, it appears as if he is still on a buying spree.” In January 1998, Business India reported, “Rubbing salt into his wound is the fact that when India Cements was passing through difficult times in 1987-89, the then IDBI chairman, S. S. Nadkarni, had requested Raju to take over the ailing company. But he had refused saying “one should not close in on a weak colleague.”

Analysts pointed out that ICL had strategic advantages in taking over Raasi. In 1997, ICL added 2.2 million tonnes per annum (mtpa) new capacity through acquisitions and expansions. The addition of Raasi's 2 mtpa capacity would make it the undisputed leader in the south of the country. Again, a Raasi takeover meant automatically acquiring 39.5% equity in the 1 mtpa Sri Vishnu Cement Ltd. (SVCL), another Group Company.

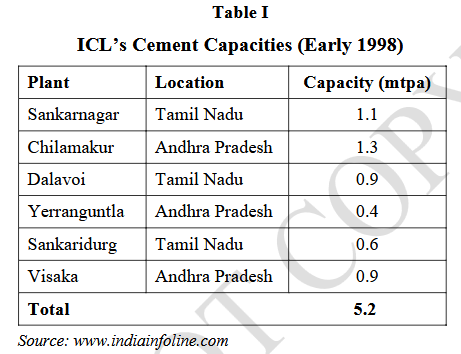

ICL was one of the largest cement producers in south India. The company had a strong presence in the states of Tamil Nadu, Kerala and Andhra Pradesh. Cement constituted approximately 97% of ICL's total revenues. Besides cement, the company had a presence in wind energy and real estate. In early 1998, ICL had six cement plants, three each in Tamil Nadu and Andhra Pradesh and its capacity had increased to 5.2 mtpa. ICL entered Andhra Pradesh by acquiring the Chilamakur plant from Coromandel Fertilizers in 1990. In September 1997, ICL took a 100% stake in Visaka Industries Ltd through its subsidiaries and associate companies. Also in 1998, ICL acquired the Yerranguntla plant from the Cement Corporation of India (CCI).

Raasi was promoted by Raju and his son-in-law, N P K Raju in 1978. Other than cement, the group also had interests in ceramics and paper. Raasi's cement division had a capacity of 1.60 mtpa.

Raasi seemed to be an attractive target for ICL as it was a relatively low cost producer. Analysts felt that Raasi failed to capitalize on its low production cost, because of its weak marketing set-up, particularly in Kerala and Tamil Nadu. As a result, Raasi tended to dump the cement in its weak markets thereby putting pressure on other players in the region. The takeover of Raasi also would help in rationalization of various markets between ICL and Raasi, and interchangeable use of Sankar, Coromandel and Raasi brand names.

Analysts felt that if ICL was indeed interested in Raasi and was buying its stock, then it was probably doing so in the belief that the family, despite Raju's assertion, would sell out. Raju had no sons, but his three sons-in-law were involved with the running of the company, and at least one of them seemed to be interested in selling out.

ICL was no stranger to Raasi. In 1995, one of Raju's sons-in-law sold the 0.68 million shares in his possession (roughly 4 per cent of the company's equity) to Srinivasan, on the understanding that the shares would be bought back in more favourable times. According to Raju this was done without his knowledge. Since then, ICL had been quietly increasing this stake. The company bought an additional 0.13 million shares in 1996-97 at an average price of Rs 90, taking its stake to around 5%. When the share dipped to Rs 50 in October 1997, it was an opportune moment for ICL to increase its holdings in Raasi and by late 1997, ICL increased its stake in Raasi to 8%.

In the late 1990?s the Indian cement industry was a highly fragmented one. There were 117 plants belonging to 59 companies spread across the length and breadth of the country, with an installed capacity of 109.97 mtpa.

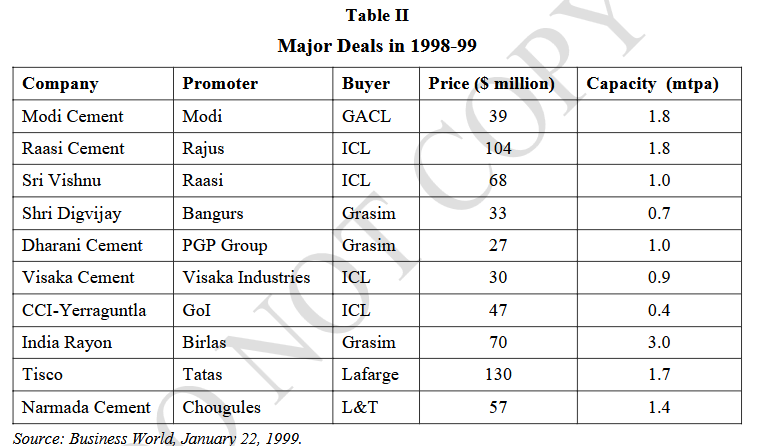

In the early 1990s, the industry expanded considerably as new plants with large capacities came up. The success of the economic reforms of the early 1990s was a boost to the expansion plans of the cement companies. However, in the mid and late 1990s, as demand for cement declined, the share prices of most companies fell. In the late 1990s, acquisitions triggered off consolidation in the cement Industry. The process of consolidation started in 1998 with ICL taking over Visaka Cement and CCI's plant at Yerraguntla, (Andhra Pradesh) and Grasim taking over Dharani Cement and Shri Digvijay Cements. Also, in 1998, Lafarge, a French building material multinational took over Tata Iron and Steel Co's (Tisco) 1.7 mtpa plant. (Refer Table II for major deals in 1998-99).

The main reason for the sudden spate of acquisitions was that overcapacity had squeezed margins, making it impossible for the smaller, inefficient players, especially in the north and west, to carry on with their operations. Capacity had grown by 9% a year, whereas demand had grown by only 7%. The industry was operating at an average capacity of 81% in 1996-97, 1% less than in the previous year. But most plants need to operate at over 85% capacity utilization to make a profit.

In contrast to the northern and western regions, in the late 1990s, Southern region had a deficit of cement. In the late 1990s, both Larsen & Toubro (L&T) and Gujarat Ambuja Cements Limited (GACL) tried to set up their private jetties in Kerala to procure shipments from their respective Gujarat plants. However, the local cement lobby thwarted their attempts, and as a result, neither L&T nor GACL was able to set up a jetty. Some supplies were transported using the Bombay Port Trust's jetty services in Kerala. But as their market prices were non-competitive, the shipments were stopped. Analysts felt that the attempts by cement producers from the north and west India to transport cement to the south was likely to meet resistance in future especially in the coastal markets.

Demand in this region was driven by the housing sector in Kerala and Tamil Nadu, and large infrastructural developmental work in Andhra Pradesh.

During the period 2000-05, demand for cement was expected to grow at 10-12% per annum. With the industry operating at 85% capacity, the regional deficit for cement in the southern region was expected to grow by 20-30% in 2000-05. Therefore, prices were expected to increase by at least 5%-6% p.a. in 2000-05.

Analysts felt that the acquisition drives by companies like ICL, Grasim, L&T and GACL in the late 1990s was only the first phase of a long awaited consolidation process in the Indian cement industry. Nowhere in the world were there 117 cement plants spread over 59 companies. They felt that the number of companies would fall to a single digit number by 2005. Companies with smaller capacity would either sell out or close down operations.

By January 1998, Srinivasan had accumulated 18.03% of Raasi?s equity, both through open market purchases as well as by buying out the stake of an estranged faction of the Raju family. In February 1998, Srinivasan announced an open offer to acquire an additional 20% of Raasi?s equity. He offered Rs 300 per share, 72.41% above the stockmarket price of Rs 174 on February 26, 1998. Raasi?s shareholders seemed to find it hard to turn down his offer. On March 1, 1998, the state-owned APIDC sold its 2.13% stake in Raasi to ICL. Subsequently, a Chennai-based stockbroker, Valampuri & Co., cornered 1.40 % of Raasi?s equity from the market for Srinivasan, taking ICL?s stake in Raasi to 21.56%. Srinivasan was also negotiating with V.P. Babaria, a transporter for both ICL and Raasi, to pick up his 7% stake in the latter. If Babaria sold his stake, ICL?s stake in Raasi would go up to 28.56%. With more than 25% of Raasi?s equity in his kitty, Srinivasan would be in a position to veto any special resolution put up for the approval of Raasi?s shareholders. A confident Srinivasan told Business Today in Chennai: “Raju cannot wish me away and that?s irrespective of the response ICL will elicit for its public offer, which will be open between April 15 and May 15, 1998.”

Unwilling to take any chances, Raju planned to execute a series of defensive manoeuvers to stall Srinivasan.

Raasi could get its shareholders to approve the hiving-off of the 39.5% stake it owned in SVCL. But this could be opposed by the financial institutions as Raasi had promised BIFR9, while taking over the sick company, that it would not dispose of the shares. Raju also had the option of making a counter-offer to his shareholders, and weaning away potential sellers from Srinivasan. But this was an expensive option, (Raju needed approximately Rs 100 crore to make a counter bid) and he did not seem to have the funds to pull it off.

Raju's efforts to find a 'white knight' didn't succeed either. R. Kunjitapadam, technical adviser and vice chairman, Raasi, said, “Some companies did try to help us out of the crisis. We were looking for assistance in the form of a white knight, or joint participation in developing the company further, and parting at a later date.” Raasi approached three sources - Kumar Mangalam Birla (Chairman, A.V.Birla Group), GACL and Switzerland?s Holder Bank. Birla wanted a 51% stake while GACL seemed to prefer a takeover. Raju then made a final attempt by talking to Holder bank, but the latter wanted to merge Raasi with its Indian enterprise, Kalyanpur Cements.

Raju expected help from the Andhra Pradesh government and other state industrialists who were against ICL?s takeover bid. However, Mr. Chandra Babu Naidu, the Chief Minister of Andhra Pradesh, refused to meet a delegation of state industrialists who wanted to present Raju?s case. His only comment to the sale of APIDC's stake in Raasi was, “The old man will be unhappy”.

In March 1998, realizing his predicament, Raju began to negotiate with Srinivasan to sell his 33% shares in the company. In an exclusive interview to Business India Raju said, “Though I had 33% of the shares and associates held 10%, I needed another Rs.1 billion for 51%. I did not want to incur further debts. It will take me ten births to repay them. Let this child of mine be happy, even if it's with a new owner.”

After protracted negotiations with an ICL team which flew down from Chennai to Hyderabad, Raasi decided to let ICL buy its shares at Rs.286 a share. In April 1998, Business World reported, “On paper Raju has reaped a harvest of Rs. 1.49 billion on this deal. But after deduction of all dues and shares for friends and relatives from the promoters? stake of 33%, Raju will net only Rs 30 million in his personal account.”

Commenting on the sell-out, Srinivasan said, “We are happy that Dr B V Raju and his associates have agreed to sell their stake in Raasi Cement. The consolidation process will be beneficial to both companies as it would result in production, marketing and distribution synergies.” “At a later date, we plan to merge both the companies”, he added.

The takeover of Raasi by ICL led to a new controversy over the ownership of SVCL. SVCL was of strategic importance to both ICL and Raju (See box). In early 1998, when ICL made known its intention to take over Raasi, it was believed that SVCL, in which Raasi had a 39.5% stake, would be part of the deal. However, when ICL came up with its open offer for Raasi, it discovered that the latter's entire stake in SVCL had been sold to some of the promoter's group companies. In late 1997, Raasi had convened a couple of board meetings and its shares in SVCL were divested at Rs10 each, allegedly to Raju's friends and relations. Till the eventual takeover was complete no one questioned this deal. After the takeover of Raasi, ICL examined Raasi?s books and found that it had violated the Securities & Exchange Board of India (SEBI) takeover guidelines which prohibited the target management from disposing off any asset during the open offer period. ICL complained to SEBI that Raasi had divested its 39.5% holding in SVCL in favour of nine firms controlled by Raju, in violation of the SEBI takeover code and the Companies Act.

Retaining SVCL was of strategic importance for both ICL and Raju. Having lost control of Raasi, Raju had no other foundation to build his empire on. On the other hand, ICL could further consolidate its presence in South India if it could control SVCL.

More important, ICL, whose Coromandel brand sold at a premium of Rs 15 to Rs 20 per 50-kg bag, could further increase its profitability by selling a part of the produce of Raasi and SVCL under the same brandname. A higher profitability would obviously reflect in a higher scrip price. That would not hurt ICL, which planned to raise money through a Rs 250-crore rights issue to part-finance the Raasi takeover.

SEBI ordered an investigation into the legality of this share transfer and the Hyderabad City Civil Court was to judge how fair the transfer was to the shareholder of Raasi. Company sources said that Srinivasan would try to convince the courts that the shares were sold at a throwaway price of Rs 10. This would make the deal detrimental to shareholders? interests under Section 397 of the Companies Act, 1956, which dealt with “prevention of oppression,” and defined oppression as “lack of probity and fair dealing in the affairs of a company to the prejudice of its members.”

In August 1998, Raju and his associates announced an open offer for a 20 per cent stake in SVCL at Rs 25 per share to increase their share from 39.5% to around 60%. On September 4, 1998, SEBI allowed Raju to go ahead with his open offer. Confident of the success of the open offer Raju increased the original offer price of Rs 25 per share to Rs 100 in September 1998. Meanwhile, in August 1998, Raju also picked up a 26.21% stake in SVCL, buying the shares of Industrial Development Bank of India (13.16%), Industrial Credit and Investment Corporation of India (6.53%), and the Industrial Finance Corporation of India (6.52%).12 With this acquisition he increased his holdings in SVCL to 65.71%.

Raju then tried to raise his stake in SVCL to over 90%. If all went well, Raju could delist the company by making another open offer to the remaining shareholders. Even if he had to return the 39.5% stake to Raasi, he would still hold a controlling stake of over 50%.

If SEBI was convinced that the share-transfer was deterimental to the interests of Raasi?s shareholders, it had two options. One, the transfer could be reversed: Raju could be legally forced to return the 39.5% stake to Raasi. Or, SEBI could direct Raju to pay the difference of Rs 90 per share to Raasi.

In mid 1999, almost a year after SEBI started its investigations, it was yet to make a public statement on what its investigations had revealed.

In October 1999 Raju sold his disputed 39.5% stake in SVCL to ICL. In a compromise reached in Hyderabad, Raju sold his shares for Rs 1.15 billion, at Rs. 120 a share. Commenting on the surrender, Raju said, "I have had a long and successful innings, but the younger generation of the family is more interested in high technology areas like software. In view of my age and keeping in mind the interest of the stakeholders in SVCL, we decided to divest in favour of ICL." With this, ICL acquired 88.55% of SVCL's paid up capital. All cases relating to the matter, pending before SEBI were dropped. In December 1999, ICL Securities Ltd. (ICLSL), along with ICL and Raasi made an offer for the purchase of the remaining shares of SVCL (constituting 11.45% of the equity share capital) at Rs. 98.25 per share. By the end of 2000, SVCL became a subsidiary of ICL.

1. “ICL had strategic advantages in taking over Raasi.” Explain in detail the advantages that ICL had in taking over Raasi.

2. The drama of the hostile takeover of Raasi abruptly ended with Raju selling out his entire stake in Raasi. Explain in brief the strategy adopted by ICL to take over Raasi.

3. The takeover of Raasi reached its logical conclusion with the takeover of Sri Vishnu Cements. Explain the significance of Sri Vishnu for both Raju and ICL. How did ICL finally win the battle for Sri Vishnu Cements?

4. In the late 1990s, the Cement Industry saw a lot of consolidation and there was a spate of acquisitions. Explain the rationale behind these acquisitions.(Make valid assumptions)

Keywords

cement industry, India, takeover, Raasi, Sri Vishnu Cement Limited, SVCL, India Cements Limited, ICL, stake, 1990, options, Business Strategy, mergers, takeovers, acquisitions, growth, expansion, geographic market-extension merger, two firms, operations, non-overlapping, geographic areas, rationalization, companies